World Center for Strategic Studies

From closed analysis to public debate

- MONTH

- YEAR

Financing the EU budget: an assessment of five proposals for new resources

A report entitled Financing the EU budget: an assessment of five proposals for new resources, that examines the efficiency of new levies for the EU budget in 2028–2034, was posted on the website of the Bruegel Institute (Brussels European and Global Economic Laboratory) on 20 April 2026.

It proposes that five new revenues should be harnessed:

1. Revenue from the Emissions Trading System (ETS)

The Commission proposes shifting 30 percent of revenues from the auctioning of emission allowances from national budgets to the EU budget. This will be done regardless of whether the allowances are auctioned or redirected to some fund. This prevents EU countries from reducing their contribution by altering auction practices.

The Commission estimates the average annual EU budget revenues at about EUR 9.6 billion for 2028-2034, based on a carbon price of EUR 88 per tonne of carbon dioxide (2025 prices). However, the actual average price for 2025 was EUR 74.20. In February–March 2026, the price fell below EUR 70. This volatility makes the expected annual revenues uncertain.

2. The Carbon Border Adjustment Mechanism (CBAM)

CBAM aims to prevent the relocation of carbon-intensive production to jurisdictions with less stringent emissions standards by applying a duty on the respective imports.

This currently accrues to national budgets, but the Commission proposes that 75 percent be allocated to the EU budget since 2028. The Commission estimates this revenue potential at up to EUR 1.2 billion annually. But the revenue could fall if exporting countries introduce their own carbon pricing systems.

3. Tobacco excise duty own resource (TEDOR)

TEDOR (at a rate of 15 percent) is to support public health and generate EU budget revenue. As the levy would be based on minimum rates, it would not mechanically raise tobacco prices. That would depend on whether EU members would raise national excise duties to offset transfers to the EU budget.

The Commission estimates the average annual revenues from TEDOR at EUR 4.9 billion over 2028–2034. However, an update to EU minimum tobacco excise rates is planned; if this is agreed, the annual revenues could rise to EUR €11.2 billion.

4. Non-collected EEE waste

The Commission proposes a levy of EUR 2 per kilo on non-collected electrical and electronic equipment (EEE). This levy would be paid directly from national budgets.

EEE-waste collection supports the EU goals of reducing health risks from hazardous substances, environmental protection, and recovery of critical raw materials such as copper, platinum and rare earth elements. The Commission projects about EUR 15 billion in revenue annually. The revenues may decline as collection rates rise.

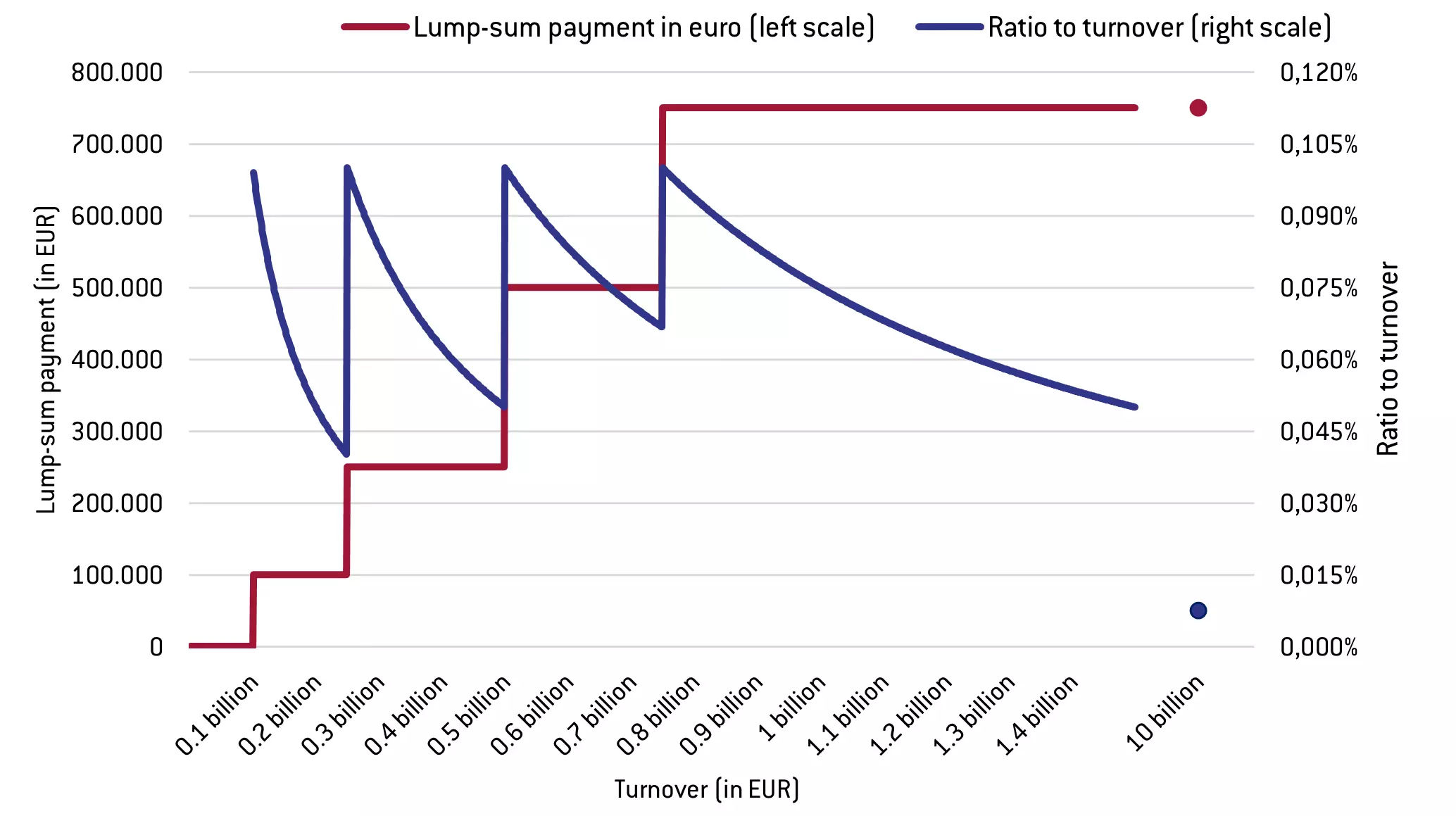

5. Corporate Resource for Europe (CORE)

CORE is a levy on companies with an annual net turnover above EUR 100 million. They would be required to pay a fixed annual levy of between EUR 100,000 and EUR 750,000, depending on their turnover bracket. The Commission argues that companies benefitting from the single market should contribute to the EU budget.

CORE fails to align with key principles of sound tax design. Turnover-based levies introduce tax cascading by taxing each production stage. This creates cumulative burdens along supply chains, encourages vertical integration and reduces economic efficiency.

The authors of the report recommend endorsing four of the five proposed new own resources – those based on ETS and CBAM revenues, tobacco and EEE waste. The fifth proposal, CORE, should be withdrawn, they say.

The Brussels analysts thus suggest retaining the levies to be shouldered by consumers directly while scrapping the tax on corporations.